Homeownership & Retirement: Securing Your Golden Years Through Real Estate

Rodd Miller, CMA, Branch Manager/ Sr. Mortgage Advisor/Reverse Division ManagerJuly 17, 2023 — 11 min read

When it comes to planning for retirement, it is essential to recognize the pivotal role that homeownership can play in securing a robust financial future throughout your golden years.

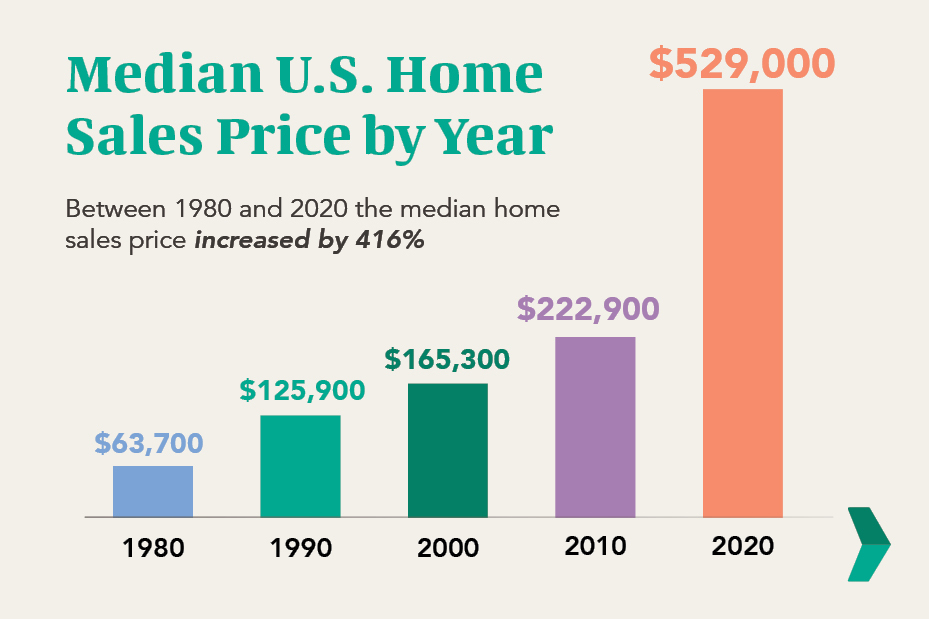

Recent studies indicate that approximately 80 percent of individuals aged 60 and above in the United States are homeowners, with housing wealth contributing to nearly half of their median net worth. This suggests that homeowners approaching retirement may possess a significant potential source of retirement income!

Real estate presents various opportunities that can yield remarkable rewards. These include building equity, generating rental income, ensuring stability for yourself and future generations, and capitalizing on potential tax advantages, among other enticing benefits. Use the tips in this blog to incorporate real estate into your retirement strategy and position yourself to reap the rewards and security of property ownership through retirement.

Benefits of Homeownership in Retirement

Equity and generational wealth. When you own a property, each mortgage payment you make contributes to increasing your equity stake in the home; over time, as the value of the property appreciates, your equity grows even further. This equity can be a valuable asset that can be tapped into to cover healthcare costs, fund major expenses, provide a safety net for unexpected events, or be passed on to future generations as part of your legacy.

Rental income and cash flow. Rental income and cash flow are significant benefits of homeownership in retirement. If you own additional properties or have extra space in your home, renting out a portion of it can provide a steady stream of rental income that can supplement your retirement savings and help cover mortgage payments, property taxes, insurance, and maintenance costs associated with the property.

RELATED: Here’s How Buying a Home Can Set You Up for Financial Success

Moreover, rental income can have even longer-term benefits—as property values increase over time, rental income has the potential to grow as well. This can contribute to building additional wealth and increasing your overall financial security in retirement. However, it's important to note that being a landlord comes with responsibilities. It involves managing the property, finding suitable tenants, collecting rent, and addressing maintenance and repair issues.

Stability and control over housing expenses. Unlike renting, where monthly payments are subject to fluctuations and potential rent increases, owning a home provides stability in housing costs. With a fixed-rate mortgage, you can enjoy consistent monthly payments throughout your retirement years, allowing for better budgeting and financial planning. In addition to stability, homeownership also offers control over housing-related expenses. While there may be ongoing maintenance and homeownership costs, you have the ability to manage and plan for these expenses.

Owning a home also gives you the freedom to customize and personalize your home according to your preferences and needs. Whether it's making renovations, creating a garden, or adapting the space to accommodate aging in place, it allows you to make decisions that enhance your comfort and quality of life in retirement.

Potential tax advantages. Owning a home can provide various tax benefits that can help lower your overall tax liability and increase your disposable income during retirement. The interest you pay on your mortgage is generally tax-deductible, meaning you can reduce your taxable income by the amount of interest paid. This can result in substantial tax savings, especially in the early years of your mortgage when interest payments are higher.

Additionally, property taxes paid on your primary residence are often tax-deductible. This allows you to further reduce your taxable income and potentially lower your overall tax burden. It's important to consult with a tax professional to understand the specific rules and limitations regarding mortgage interest and property tax deductions in your jurisdiction.

Furthermore, if you decide to sell your primary residence in retirement, there may be potential tax benefits. In the United States, for example, homeowners can benefit from the capital gains exclusion. If you have lived in your home for at least two of the past five years before selling, you may be eligible to exclude a portion of the capital gains from taxation. This can result in significant tax savings when selling a home that has appreciated in value.

RELATED: What Are the Tax Benefits of Owning a Home?

Factors to Consider When Planning for Retirement with Real Estate

- Evaluate your finances and long-term goals. The first step is to understand your complete financial footprint, including retirement savings, debts, and ongoing expenses; then, you must define your retirement goals, such as your desired lifestyle, location, and financial security. This evaluation will guide your real estate decisions.

- Select an appropriate property. Next, you must determine whether a primary residence, rental property, or downsizing best aligns with your retirement plans. Each option has different financial implications, so consider the potential income, maintenance costs, and the impact on your lifestyle.

- Determine affordability and manage mortgage debt. Proceed by examining your retirement income sources, such as pensions, Social Security benefits, and investment returns. Calculate the amount of money you will have available on a monthly basis to cover housing expenses. Next, assess your savings and determine how much you are willing and able to allocate towards a down payment. A higher down payment can help reduce the overall mortgage amount and potentially lead to lower monthly payments. However, it's essential to strike a balance between putting in a significant down payment and ensuring you have enough savings for other retirement needs.

- If you plan to carry a mortgage into retirement, carefully assess the terms, interest rate, and repayment period of the loan; aim to secure a mortgage with favorable terms that align with your financial situation and retirement goals. Regularly review your mortgage debt and consider strategies to pay it off before or during retirement.

- Factor in maintenance and homeownership costs. Finally, owning a home comes with ongoing expenses beyond the mortgage payment; as a homeowner, you are responsible for addressing issues that arise, such as fixing plumbing, electrical, or structural problems. It's important to budget for these maintenance costs and set aside funds to cover unexpected repairs that may occur. Homeownership costs also encompass property taxes, insurance premiums, and homeowners association (HOA) fees, if applicable.

RELATED: Your ‘No Sweat’ Summer Home Maintenance Checklist

Strategies for Incorporating Real Estate into Retirement Planning

Pay off your mortgage before retirement. If it seems feasible, make it a goal to pay off your mortgage before retirement; allocate extra funds towards your mortgage principal, consider biweekly payments, or explore refinancing options to accelerate debt repayment. If you have additional income or windfalls, consider using them to make extra payments towards your mortgage principal. By paying down the principal, you can reduce the amount of interest you pay over the life of the loan and accelerate the process of becoming mortgage-free.

RELATED: Strategies to Pay Off Your Mortgage Early: Achieving Financial Independence Sooner

Downsize to a smaller, more affordable space. This can have several financial benefits, including:

- Reduced housing expenses: Downsizing typically results in lower housing costs, including mortgage payments, property taxes, and insurance expenses.

- Unlocking home equity: When you downsize, you may be able to sell your current home at a higher price than what you paid for it. The difference between the sale price and your mortgage payoff, minus transaction costs, represents the home equity that you can potentially use to bolster your retirement savings or invest.

- Lower maintenance and upkeep: With fewer rooms and a smaller yard, you can reduce expenses associated with cleaning, repairs, and landscaping.

Before downsizing, assess your space requirements and consider what you truly need in retirement.

RELATED: Making the Move: Exploring the Benefits of Downsizing Your Home

Rent out a portion of your property for additional income. If you have extra space in your home or own additional properties, here's how renting out a portion of your property could benefit you:

- Steady rental income: By renting out a portion of your property, such as a spare room, basement, or an accessory dwelling unit (ADU), you can generate a steady stream of rental income. This additional income can supplement your retirement savings, cover mortgage payments, property taxes, insurance, and maintenance costs associated with the property.

- Potential for long-term growth: As property values appreciate over time, the rental income from your property has the potential to increase as well. By staying informed about local rental market trends and adjusting rental rates accordingly, you can capitalize on market demand and potentially earn even higher rental income in the future. This can contribute to building additional wealth and increasing your overall financial security during retirement.

- Flexibility and control: Renting out a portion of your property gives you the flexibility to decide how much space you want to rent and for how long. You can tailor your rental arrangement to meet your needs, whether it's short-term rentals, long-term leases, or even utilizing platforms like Airbnb for vacation rentals.

Utilize home equity through a reverse or home equity mortgage. Utilizing home equity through a reverse mortgage or home equity loan is another strategy for incorporating real estate into your retirement planning. These financial tools allow you to tap into the value of your home and access the equity you have built up over the years.

The benefits of a reverse mortgage include:

- Supplementing retirement income: By receiving regular payments or a lump sum, a reverse mortgage can provide you with additional income to cover daily expenses, healthcare costs, or other financial needs.

- No monthly mortgage payments: With a reverse mortgage, you are not required to make monthly mortgage payments. Instead, the loan balance accumulates over time and is repaid when the home is sold. This can alleviate financial strain during retirement when cash flow may be limited.

- You retain ownership of your home: With a reverse mortgage, you continue to own your home, and you can live in it as long as you fulfill the loan requirements, such as maintaining the property and paying property taxes and insurance.

MORE INFO: Click Here to Find Out If You’re Eligible for A Reverse Mortgage

The benefits of a home equity loan include:

- You have access to a large sum of money: A home equity loan allows you to access a substantial amount of money upfront, which can be beneficial if you have a specific financial goal or need in mind.

- Lower rates: Home equity loans often have lower interest rates compared to other forms of borrowing, such as credit cards or personal loans, making them an attractive option for financing major expenses.

- Fixed monthly payments: With a home equity loan, you know exactly how much you need to repay each month, making it easier to budget and plan your retirement finances.

RELATED: Unlock Potential: How a HELOC Can Help You Invest in Real Estate

Risks & Challenges When Planning for Retirement with Real Estate

While incorporating real estate into your retirement planning offers numerous benefits, it's crucial to be aware of the risks and challenges involved. Here are some key factors to consider:

- Market fluctuations. Real estate values can experience fluctuations over time due to economic and market factors. Changes in interest rates, local market conditions, and broader economic trends can impact property values.

- Property management. Owning rental properties or even your own home requires diligent property management and ongoing maintenance. This includes regular upkeep, repairs, and handling tenant-related matters. It's essential to be prepared for the time, effort, and financial resources required to effectively manage and maintain the property and protect your investment.

- Potential rental income or tenant issues. Renting out a property comes with the risk of encountering problematic tenants who may cause damage, violate rental agreements, or be unreliable with rent payments. It's crucial to conduct thorough tenant screenings, establish clear rental agreements, and be prepared to address any issues that may arise. Additionally, vacancies or late payments can impact your rental income, so it's important to have contingency plans and financial buffers in place.

- Impact of location. Finally, the location of your property can significantly impact its value and rental income potential. It’s important to research and choose properties in areas with stable or growing real estate markets to minimize the risk of declining values and maximize the potential for appreciation.

Take a Confident Next Step with Advice You Can Trust

You’ve worked hard and deserve the chance to secure a strong financial future. Get started with a customized quote today, or reach out to your neighborhood Mortgage Advisor here.

Categories

Archives

Recent Posts

- No Down Payment for First-Time Homebuyers

- How Does A 30-Year Mortgage Work: A Simple Guide

- Your Comprehensive Homebuying Checklist: A Step-By-Step Guide

- Mortgage Pre-Approval: Everything You Need to Know

- What Are the Benefits of a USDA Loan for Homebuyers?

- How Many People Can Be On A Home Loan? Your 2024 Guide

You bring the dream. We'll bring the diagram.

There’s a financing solution for just about every situation.

I felt like I was treated like family, great communication and helping me with any questions I had.

You bring the dream. We'll bring the diagram.

There’s a financing solution for just about every situation.

Where does your sun shine? Find your local advisor.

Enter your city or state to see advisors near you.