School's in Session: Mastering the ABCs of First-Time Home Buying

David Boliard, Branch Manager/Sr. Mortgage AdvisorAugust 7, 2023 — 15 min read

Purchasing a home for the first time is an exciting milestone, marking a significant step toward financial independence and stability;

While it may seem daunting at first, full of weird terms and complicated procedures, it's possible to navigate with confidence and ease if we break the process down into manageable components.

Whether you're considering buying a cozy townhouse or a sprawling suburban property, this blog will serve as a comprehensive guide to purchasing your first home and setting yourself up for a strong financial future.

The Building Blocks of Homebuying

Before plunging into the home-buying process, it’s important to grasp core concepts and key terminology that will form the building blocks of your journey. Let's explore foundational terms that you'll encounter throughout this process and unpack their significance.

First and foremost, let's discuss the down payment:

- This refers to the money you pay upfront when purchasing a home. It’s typically calculated as a percentage of the total purchase price and serves as a sign of your commitment to the property.

- In general, a larger down payment indicates a lower loan-to-value ratio, which means you are borrowing a smaller percentage of the total purchase price. This lower ratio can lead to more favorable loan terms, including lower interest rates and potentially avoiding the need for private mortgage insurance (PMI).

- The percentage required for a down payment varies depending on factors such as the type of loan, your financial situation, and the lender's requirements; however, it is common for down payments to range from 3% to 20% of the purchase price.

For example, if you're buying a home worth $300,000 and the down payment requirement is 10%, you would need to pay $30,000 upfront.

Saving for a down payment is often one of the biggest challenges for first-time homebuyers. Establishing a budget and allocating a portion of your income towards a down payment fund may be helpful. Additionally, exploring programs and initiatives available to first-time buyers, such as government-assisted down payment assistance programs or grants, can provide valuable support in achieving your homeownership goals.

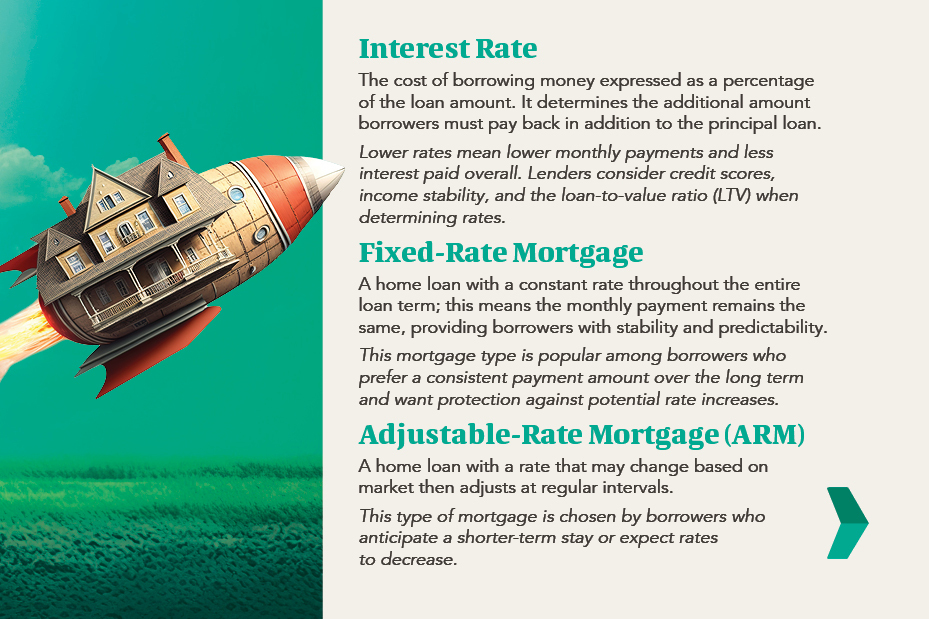

Interest rates are another crucial aspect of buying a home:

- The interest rate is the percentage charged by the lender on the amount borrowed, determining the overall cost of the loan.

- Rates can vary over time due to several factors, including economic conditions, inflation rates, and central bank policies. It's important to stay informed about market trends and economic indicators that can give you insight into the direction of interest rates.

- Securing a mortgage with a lower interest rate can result in significant long-term savings, as even a fraction of a percentage point difference in the interest rate can add up to thousands of dollars in savings over the life of your mortgage.

For example, on a 30-year mortgage of $250,000, a decrease in the interest rate from 4% to 3.5% could save you approximately $26,000 in interest payments.

- RateSafe*, our interest rate lock, confirms the interest rate we offer you will stay the same for 120 days. This is a valuable tool for borrowers who are still searching for the perfect space but want to secure a competitive rate throughout their loan application and approval process. Click here to learn more.

To ensure you secure the most favorable terms for your mortgage, it's essential to maintain a good credit score; additionally, it's worth exploring the different types of mortgage options available and understanding how they may impact your interest rate.

Fixed-rate mortgages offer stability, as the interest rate remains constant throughout the loan term. On the other hand, adjustable-rate mortgages (ARMs) have interest rates that can fluctuate periodically, usually after an initial fixed-rate period. ARMs may offer lower initial interest rates but can pose risks if rates rise significantly in the future.

RELATED: Fixed-Rate vs Adjustable-Rate Mortgages

Basic terms to keep in mind when learning about interest rates:

Lastly, closing costs are expenses incurred during the final stages of the home-buying process:

- These can include a range of expenses, so it's crucial to be aware of them and plan for them in advance.

- It's important to note that closing costs can vary significantly depending on factors like the location of the property, the purchase price, and the specific loan terms.

Basic terms to keep in mind when learning about closing costs:

- Home appraisal fee. Before finalizing the mortgage, lenders often require a professional appraisal of the property to determine its fair market value. This appraisal fee covers the cost of the assessment and ensures that the property's value aligns with the loan amount.

- Title search and title insurance. A title search is conducted to verify that the property's title is clear of any liens, disputes, or legal issues. Title insurance protects the buyer and the lender from any potential claims or defects in the property's title. Both the title search and title insurance involve fees that contribute to the closing costs.

- Attorney fees. In some cases, it may be advisable or required to hire an attorney to oversee the closing process and ensure all legal aspects are properly handled. Attorney fees are typically incurred to ensure a smooth and legally sound transaction.

- Lender fees. Lenders may charge various fees related to loan processing, underwriting, and origination. These fees can vary between lenders and can significantly contribute to the overall closing costs.

- Escrow fees. Escrow services are often utilized during the closing process to hold and disburse funds securely. Escrow companies charge fees for their services, which are typically divided between the buyer and the seller.

- Prepaid expenses. Some closing costs include prepaid expenses, such as property taxes, homeowner's insurance premiums, and prepaid interest. These expenses ensure that the buyer's escrow account is properly funded and that necessary payments are made.

Exploring Your Homeownership Goals and Needs

When embarking on the journey of homeownership, it's crucial to take the time to determine your personal needs and goals. This step sets the foundation for finding the perfect home that aligns with your lifestyle, preferences, and long-term plans.

Location. This should be one of your first considerations when defining your homeownership goals. Consider what may be the ideal neighborhood for you now versus in the future. Factors such as proximity to your workplace, quality of schools, access to amenities, and overall community vibe also play a significant role in choosing the right location for you.

Property type. This is another important aspect to think about—do you imagine living in a single-family house, a townhouse, a condo, or a multi-family dwelling? Each property type offers its advantages and considerations, so it's essential to evaluate what aligns with your preferences and requirements. Consider factors such as maintenance responsibilities, privacy, shared amenities, and future expansion possibilities when making this choice.

Property size. When it comes to buying a home, size matters—assess what you need now versus what you may need in the future in terms of bedrooms, bathrooms, living space, and outdoor areas. Consider factors such as the size of your household, potential growth or changes in family dynamics, and any specific requirements you might have, such as a home office, a dedicated play area, or space for entertaining guests.

Once you’ve identified your goals, it’s crucial to evaluate needs versus wants. Distinguishing between essential features and desirable but non-essential ones helps you prioritize your preferences and make more informed decisions. Create a list of must-haves that align with your lifestyle, functionality, and long-term goals. This could include factors such as the number of bedrooms, a fenced backyard, a specific school district, or a certain architectural style. Differentiate these from the features that would be nice to have but are not deal-breakers, such as a swimming pool, a gourmet kitchen, or high-end finishes.

Navigating the Home Search Process

You’ve done the footwork—now, it’s time to find your dream home! The search process involves several key steps, and in this section, we will outline them to help you navigate this important phase successfully. Additionally, we will provide tips on how to stay organized and focused throughout the search for your ideal home.

Get pre-approved for a mortgage. Being pre-approved for a mortgage gives you a clear understanding of your budget and the price range of homes you can consider, which will help narrow down your search and focus on properties you can afford. Additionally, being pre-approved demonstrates to sellers that you are a serious and qualified buyer, which can strengthen your negotiating position.

It's important to note that being pre-approved is not the same as being pre-qualified. Pre-qualification is a preliminary assessment based on self-reported information; pre-approval involves a more thorough evaluation and verification of your financial details.

RELATED: The Power of Pre-Approval: How to Make Getting a Mortgage Easy and Safe

Do some research online. Utilize real estate websites and property listing platforms to explore available homes in your desired area and within your specified criteria. Take advantage of advanced search filters and features that allow you to narrow down your options and save listings for future reference.

Connect with a knowledgeable and experienced real estate agent. Collaborating with a professional who understands your needs and has in-depth knowledge of the local market can provide valuable insights and guidance. An agent can help you identify suitable properties, schedule showings, and negotiate on your behalf. They can also offer expertise in assessing the value, condition, and potential of the homes you visit.

Check out some open houses. Open houses provide an opportunity to ask questions, gather additional information, and assess the neighborhood and surrounding amenities. Take notes, capture photos, and keep a record of your impressions to help you compare and evaluate properties later.

Consider “sleeper costs”. Sleeper costs include things like homeowner's insurance, property taxes, association dues, yard maintenance, utilities, and repairs, among others. It's crucial to include these sleeper costs in your budgeting process to accurately assess the financial responsibilities that come with homeownership. By accounting for these expenses, you can ensure that you have sufficient funds to cover not only your mortgage payment, but also the additional costs associated with maintaining and protecting your property.

Understanding the Ins and Outs of the Purchase Agreement

Once you’ve found the perfect home, it's time to make an offer. The purchase agreement outlines the terms and conditions of the transaction, and understanding its components is crucial.

The most essential aspect of a purchase agreement is a contingency; these are conditions that must be met for the sale to proceed. Common contingencies include home inspection, appraisal, financing, and the sale of your current home. These clauses allow you to protect your interests and provide an opportunity to negotiate repairs or adjustments if issues arise during the inspection process.

RELATED: What is a Mortgage Contingency? Your Safe & Simple Guide

Earnest money is a deposit that demonstrates your commitment to the purchase. It serves as a show of good faith and is typically held in an escrow account until closing. The amount of earnest money can vary, but it is often a percentage of the purchase price. Should the transaction fall through due to a failure to meet the contingencies or other specified circumstances, the earnest money may be returned to you. However, if you back out without a valid reason, the seller may be entitled to keep the earnest money. Carefully consider the amount of earnest money you are comfortable offering as part of your purchase agreement.

RELATED: What is Earnest Money, and How Much Do I Need?

Crafting a competitive offer requires careful consideration of your personal circumstances and budget. Research recent comparable sales in the area to understand the market value of the home you are interested in. Your real estate agent can provide insights into local market conditions and assist you in formulating a competitive offer.

Negotiation strategies may also play a significant role in this process. Your agent can help you navigate negotiations with the seller, ensuring your interests are represented. Understand the seller's motivations, such as their desired timeline or need to sell quickly, and use this information to tailor your negotiation strategy. Be prepared for potential counteroffers and consider factors beyond the purchase price, such as contingencies, repairs, or closing costs. Effective communication and flexibility can be key in reaching a mutually beneficial agreement.

Exploring Mortgage Options to Find the Best Fit

Understanding the different types of mortgages and loan programs available can help you make an informed decision that aligns with your long-term financial goals.

Conventional loans are a popular choice for many first-time buyers. These loans are not backed or insured by the government and are offered by private lenders. The eligibility criteria for conventional loans typically include a good credit score, stable employment history, and a down payment of at least 3 percent. Click here to learn more.

FHA loans, insured by the Federal Housing Administration, are designed to make homeownership more accessible, particularly for buyers with limited down payment savings or lower credit scores. The eligibility criteria for FHA loans are generally more lenient compared to conventional loans. They require a down payment as low as 3.5% and may consider lower credit scores. FHA loans also provide the option of a fixed-rate or adjustable-rate mortgage. Click here to learn more.

VA loans, backed by the U.S. Department of Veterans Affairs, are available to eligible veterans, active-duty service members, and surviving spouses. These loans offer unique benefits, including no down payment requirement, no private mortgage insurance, and competitive interest rates. Click here to learn more.

USDA loans, insured by the U.S. Department of Agriculture, are designed to promote homeownership in rural communities; the eligibility criteria focus on the location of the property and the buyer's income. To qualify, the property must be located in a designated rural area and the buyer's income must fall within specified limits. One key benefit of a USDA loan is the option for 100 percent financing, which can be a significant advantage for first-time buyers who may be building their savings for a down payment. Click here to learn more.

Non-Qualifying (Non-QM) loans are a special kind of mortgage program that caters to borrowers who may not meet the stringent requirements of traditional mortgage loans. They’re designed to help buyers with unique financial circumstances, such as self-employed individuals, retirees, or individuals who are still building their credit. Non-QM loans consider alternative factors beyond credit or income verification, such as asset-based income, bank statements, or past payment history. Click here to learn more.

PacRes Mortgage also offers Down Payment Assistance programs. Click here to learn more or reach out to your neighborhood Mortgage Advisor.

Conducting Home Inspections and Appraisals

When it comes to the home buying process, due diligence plays a crucial role in ensuring that you make an informed decision and protect your investment. Two essential components include home inspections and appraisals. Understanding the importance of these processes and knowing what to expect can help you navigate them with confidence.

Home inspections involve evaluating the condition of the property you intend to purchase. In most cases, you will want to hire a home inspector to thoroughly assess the systems and components of the house. During the inspection, the inspector will examine things like:

- The structure and foundation of the home

- Electrical and plumbing components of the home

- The HVAC (heating, ventilation, and air conditioning) system

- The roof

RELATED: Bad Home Inspection? Here Are Your Next Steps

The inspector will identify any existing or potential issues and provide you with a detailed report. The importance of this report cannot be overstated. It allows you to make an informed decision about proceeding with the purchase, negotiate repairs or price adjustments, or even reconsider your offer if significant issues are uncovered.

Appraisals involve evaluating factors like property's condition, location, comparable sales in the area, and market trends to arrive at an unbiased and accurate valuation. This serves several purposes, including:

- Protecting the buyer and the lender by ensuring that the property is worth the amount being financed.

- Providing a basis for determining the maximum loan amount the lender is willing to offer; if the appraisal comes in lower than the agreed-upon purchase price, it may require renegotiation between the buyer and seller or additional down payment from the buyer.

RELATED: Making the Right Move: Appraisal Mistakes to Avoid

Navigating the Closing Process with Confidence

The closing process is the final step of your home buying journey, where all the necessary paperwork and financial transactions are completed to transfer ownership of the property.

One of the key aspects of the closing process is reviewing and signing the closing documents. These documents include the loan agreement, the mortgage note, the deed of trust, and other legal and financial disclosures. It's essential to carefully review these documents, ensuring that they accurately reflect the terms and conditions agreed upon during the negotiation process.

RELATED: Understanding Closing Costs: Planning for the Financial Aspects of Homeownership

One other crucial element is securing homeowner’s insurance before finalizing the mortgage; before closing, select a policy that suits your needs and budget. Coordinate with your insurance provider to ensure that the coverage is effective from the closing date.

Finally, it may also be important to conduct a final walk-through of the property before closing. This allows you to verify that any repairs or agreed-upon changes have been completed and that the property is in the expected condition. If any issues arise during the walk-through, discuss them with the seller or their representative to reach a resolution before closing.

It’s important to note that factors such as financing issues, title complications, or unforeseen repairs can cause delays. Do your part to ensure a smooth process by communicating with your lender to complete all necessary paperwork and ensure the funds are available for the purchase. Having patience and being prepared to address any hurdles will help you navigate through these situations smoothly.

What’s Next?

No two home-buying journeys are the same. If you have questions or want to talk through your options, reach out to a neighborhood Mortgage Advisor today, or click here to explore other recent blogs.

Keywords:

Categories

Archives

Recent Posts

- No Down Payment for First-Time Homebuyers

- How Does A 30-Year Mortgage Work: A Simple Guide

- Your Comprehensive Homebuying Checklist: A Step-By-Step Guide

- Mortgage Pre-Approval: Everything You Need to Know

- What Are the Benefits of a USDA Loan for Homebuyers?

- How Many People Can Be On A Home Loan? Your 2024 Guide

You bring the dream. We'll bring the diagram.

There’s a financing solution for just about every situation.

I felt like I was treated like family, great communication and helping me with any questions I had.

You bring the dream. We'll bring the diagram.

There’s a financing solution for just about every situation.

Where does your sun shine? Find your local advisor.

Enter your city or state to see advisors near you.