Loan Products

Loan Products

First-time buyer to experienced homeowner, let us help you find the perfect loan for your life and long-term goals.

CONVENTIONAL

Stable monthly payments for borrowers with solid credit profiles.

VA

Mortgage solution made specifically for military veterans, active-duty, or surviving spouses.

FHA

Affordable homeownership with a low down payment and monthly payment options.

JUMBO

Finance a home with a price that exceeds the conventional loan limit.

NON-QM

I need a home loan but don’t meet the requirements to be considered for a qualified mortgage.

USDA

I want to bring my rural dream home to life.

REVERSE

I want to unlock equity and supplement my retirement income.

RENOVATION

I want to renovate my home.

DOWN PAYMENT ASSISTANCE

Down payment assistance for first-time buyers.

CONVENTIONAL

I want to replace my current mortgage with a new loan that has more favorable terms.

VA

I want to refinance my VA loan to receive a lower monthly payment.

FHA

Looking to refinance your home quickly and easily with limited documentation?

CASH-OUT

I want to borrow against the equity in my home to consolidate debt, fund a home project, or cover unexpected expenses.

STUDENT LOAN CASH-OUT

Use home equity to pay off student loans, consolidate debt, or receive a lower monthly payment.

2ND MORTGAGE

I want to use the equity I’ve built up in my home for a renovation, to consolidate debt, cover education costs, or to pay for other large expenses

OUR NEIGHBOR COMMUNITY LENDING PROGRAM

Improved pricing in qualifying neighborhoods

OUR NEIGHBOR COMMUNITY LENDING PROGRAM

Improved Pricing in Qualifying Neighborhoods

PacRes Homebuying Process

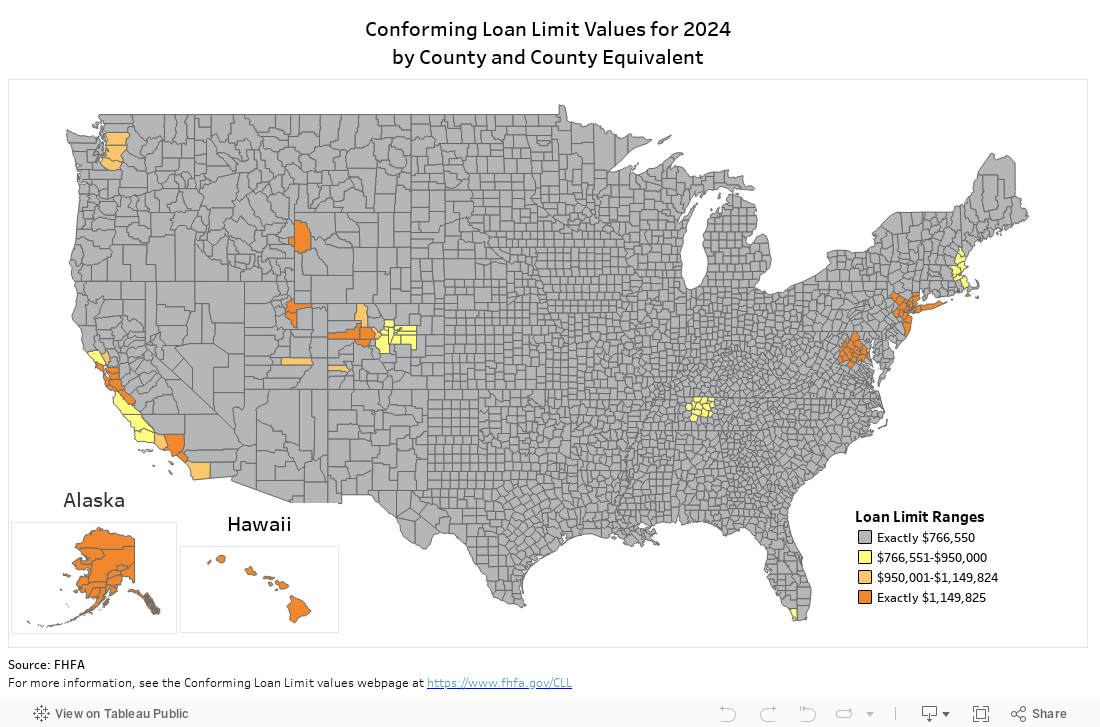

Conforming Loan Limit Values Map

Use our interactive map to find out the conforming loan limit in your neighborhood.